ISAs and the income challenge

Mixed Blessings for Savers

With the start of the new tax year, the ISA allowance has increased from £15,240 to a full £20,000. This is not only the highest it has ever been, but provides savers with a meaningful additional amount that they can shelter from tax.

In fact the combination of increases in the ISA limits, and continuing decreases in the pension contribution limits have led to many commentators to describe ISAs as “the new pension pot”.

One must, however, question if, in the current ultra-low interest rate environment, ISAs make sense for investors looking to earn income and ‘protect’ their savings from inflation?

Limited options for yield seekers

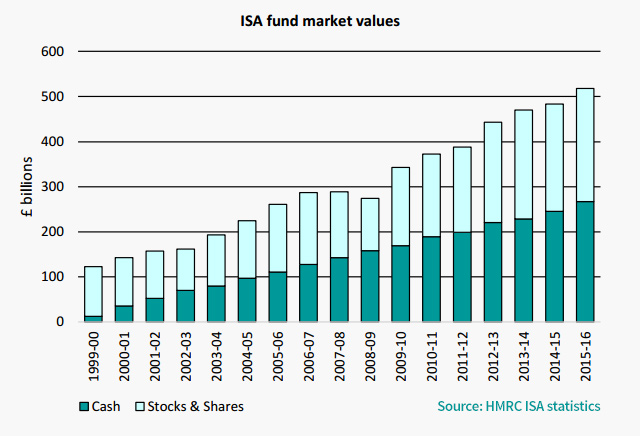

The majority of funds in ISAs are held in cash, with approximately £270 billion currently held in Cash ISAs.[1]

However, returns in Cash ISAs are at historic lows. A survey of the market shows that nearly 85% of variable rate cash ISAs are offering rates below 1.0%, with the highest rate available for a 1 year fixed-rate account still only 1.2%[2]. Recent analysis by the Telegraph suggests the best accounts are paying a third less in March 2017 than they were in September 2016.[3]

With inflation currently running at 2.3% ISA savers are losing money in real terms, even with the tax break on the income generated. To illustrate this, even if the entire Cash ISA market switched into the best accounts paying 1.2% interest, we would still see almost £3 billion of value eroded from Cash ISA savers by inflation this year.

Cash ISAs are of course not the only option for investors searching for income: Stocks and Shares ISAs, which are home to 48% of all ISA funds, are also able to invest in fixed income products such as bonds, as well as company shares. However, investors in traditional fixed income markets are also struggling to find attractive returns. NS&I calculates that the average available three year fixed term product has a rate of 1.24%[4], with the highest yielding three year fixed rate bond available on MoneySuperMarket offering a rate of 1.9%. The NS&I also notes that in the decade before 2009, the average one year fixed term savings rate was 5.0% compared to a current rate of 0.6%.

An Alternative Option for Investors Seeking Income

Another option has recently become available to investors seeking income, with the launch of the Innovative Finance ISA (‘IFISA’), in April 2016. The IFISA was originally designed to allow investors to invest in peer-to-peer loans tax free, but since November 2016, the remit was expanded to include debentures and crowd bonds, and this has expanded the options now available to investors.

The IFISA market is still in its infancy and there are fewer providers operating in the IFISA space than in the more traditional ISA sectors. However, more and more experienced investment managers are beginning to offer products that are eligible for the IFISA, enabling investors to obtain fixed interest rates sometime exceeding 5%, although the risks will be higher than with pure cash holdings. One such provider is Triple Point Investment Management, whose Advancr Secured Bond offers a fixed rate of 6.2% for a three year bond.

IFISA rates can be attractive, though investors should consider them to be investments rather than as savings.

We are living in a historically low interest rate environment, which many analysts expect to continue for the foreseeable future – investors seeking to grow the value of their savings should be considering alternative approaches with their ISAs.

Triple Point Advancr Bonds

Triple Point Advancr offers fixed-term secured bonds targeting high annual returns and are built around a simple idea; to give individual investors direct access to our professionally managed leasing and lending investments via fixed interest secured bonds.

Advancr Bonds are distinctive because each single bond is still diversified across over 50,000 underlying assets, helping to mitigate risk.

Investors can choose from a number of investment terms, income options and can also earn tax free interest by buying our Advancr Bonds through Triple Point’s Advancr Innovative Finance ISA (IFISA) or through selected Self Invested Personal Pensions (SIPPs).

Risk Warning: remember that Advancr Bonds are investments, not savings, and your capital and interest are at risk. Tax treatment depends on individual circumstances and is subject to change. Your capital will be tied up for a fixed term, and past performance is not a reliable guide to future returns.

Sources:

- HMRC Individual Savings Account (ISA) Statistics, August 2016

- Newcastle Building Society

- Telegraph Money

- FT Advisor